When life presents challenges, it’s easier to look the other way. But if troubles are out of mind and focused on something else, well, that’s a momentary win. Repeat this process enough and it’s easy to habituate looking the other way. As harmless as this sequence may seem, it’s a guaranteed path toward denial.

Let’s look at why wishful thinking can’t beat debt and why real plans—despite the anxiety they bring—will ultimately change your life.

Playing the Lottery

Americans spent $73.5 billion on lottery tickets last year. But the truly sad reality is that many of those dollars came from people who couldn’t afford it, which is wishful thinking at its worst. When debt takes over lives, the search for a quick solution ensues. The lottery fills this hopeless void too perfectly, offering life-changing potential without ever having to deliver on that potential. If you’re an optimist by nature and play the lottery with any amount of debt, please stop. After all, even if you won, there’s no guarantee your life would improve.

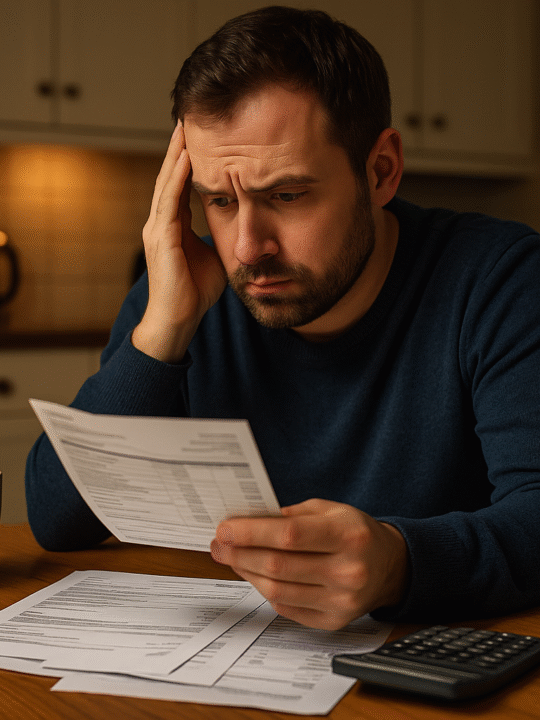

Ignoring Late Statements & Creditor Calls

Tuning out is a common coping strategy to deal with stress and trauma. When creditors are ringing daily and non-stop late notices arrive in the mail, stress builds to the point where we can do nothing sit inactive. This is the worst thing we could possibly do though. The phone will keep ringing,, more late notices will arrive, more interest will accumulate — you might even get sued by your credit card company or a collection agency. Worst of all, you won’t be cut any slack because you took no initiative to call your creditors and restructure your debt.

Fleeing Abroad

Leaving the country in the wake of overwhelming debt can sound attractive, especially in the initial shock moments of you believing your financial life is destroyed and you’ll never have another moment of happiness. But your problems will probably only compound by running away.

That’s not to say there aren’t ways to achieve a new, debt-free life in another country, but you’ll need cash to get there, cash to continue living there, and the IRS won’t forget about you, potentially treating your unpaid debts as income unless you demonstrate a reason for exclusion.

Not Recognizing What You’re Paying in Interest

According to the National Bureau of Economics Research, many people pay little attention to interest rates, with a study finding only 10 percent of people in the UK with multiple credit card balances repay their debt in the most efficient way. Not knowing the money being lost to interest in specific terms slightly alleviates the perpetual feeling of drowning in debt. This is a surefire method for spending a lifetime in debt.

Facing Your Debt Head On

Problems cannot be overcome unless the root of their cause is met head on through awareness and action. Digging yourself out of big debt affords you three options:

1) Asking Family

Certainly not an option for many people stuck in debt, but you’re close with people whom are in a financial position to help, there’s no shame in swallowing your pride and asking for assistance. It doesn’t have to be a giveaway, maybe set a reasonable payment plan with them. At the least you’ll have legal pressure off you and save yourself a lot of money in interest.

2) Declaring Bankruptcy

Declaring bankruptcy is a big step, but if you have little in the way of options, it’ll start the road to your new financial life. If you don’t have the income to make payments on your debt, declaring Chapter 7 will liquidate your assets to help pay back your outstanding debt. If you have income coming in, declaring Chapter 13 lets you keep your personal assets and forgive your debt if you can make court payments for 3-5 years.

3) Seeking Debt Relief Options

Debt relief is a viable alternative to bankruptcy, especially if you don’t want to go through the process and expense of hiring an attorney and paying court costs. Generally speaking, debt relief will involve either debt consolidation or debt settlement. Debt consolidation works to pay off multiple card balances by taking out one loan with a lower interest rate, thereby simplifying the process for a debtor while saving money on interest long-term.

Debt settlement involves a company negotiating with a consumer’s creditors to lower the percentage of their balance. The strategy often entails saving enough money while foregoing payments, then offering a creditor a lump-sum amount. According to Freedom Debt Relief reviews and FAQs, no debt settlement company should ever guarantee a certain amount (or any) savings. If a company tries to charge you fees up front, it’s a scam. Debtors should only pay fees after a debt has been successfully lowered and they’ve agreed to the debt settlement plan.

If you’re deep in debt, you have a serious problem. But if you face your problems directly instead of fill your psyche with wishful thinking that’ll never help, your troubles will only get worse. Steering clear of the pitfalls above while exploring plans that will help you get back on your feet is your best course of action.